Buying a Property in Singapore With Analytical Precision

Not Just a Property but the Right Property.

Most buyers start with a property they like and then try to justify it financially. At Own It Real Estate, we reverse this and run a rigorous macro and micro research, a five-factor ASSET score, and a comparative analysis across all shortlisted options before you make any decision.

Buying Property in Singapore Is Not a Simple Decision.

property buyers we specialise in guiding

Whether you're a first-time private property buyer, an investor evaluating a new launch, or a buyer navigating the HDB-to-private transition — the biggest mistake is starting with emotion before completing the analysis. Own It's role is to ensure your decision is grounded in data first.

01

First-Time Private Property Buyer

Making the move from HDB or renting to your first owned private property. You need clarity on what you can actually afford, which regions offer the best value, and how to evaluate a property you'll likely hold for 5–10 years.

02

Property Investor

Buying a second or third property for capital appreciation or rental yield. You need a disciplined scoring framework to compare options objectively — supply/demand dynamics, transformation potential, and safe entry price analysis.

03

Upgrader Buying Their Next Property

You've sold your previous property and are now deploying proceeds into your next purchase. Timing, quantum, and property selection all need to align with your financial plan — not just your preferences.

The ASSET Scoring proven Framework

A Five-Factor Score

for Every Shortlisted Property

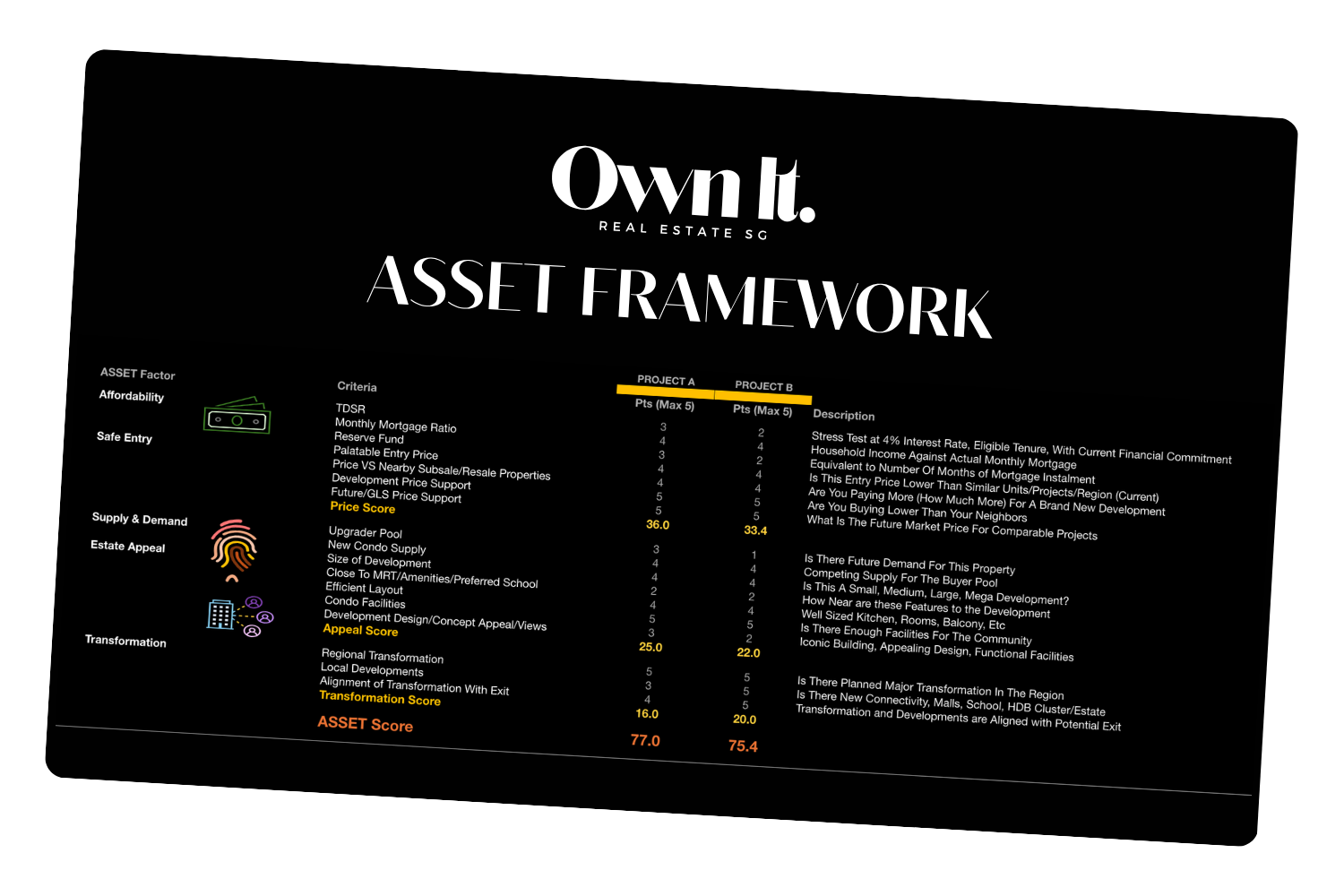

Before any offer is made, every shortlisted property is run through Own It’s ASSET framework with five weighted dimensions that produce a comparable score across all options.

You see how each property stacks up side by side, in numbers, before making a decision based on anything else.

A

Affordability

Can you sustain this financially — stress-tested and with a reserve fund built in?

- TDSR stress-tested at 4% interest rate

- Monthly mortgage as % of household income

- Reserve fund of 6–24 months of mortgage instalments

S

Safe Entry

Is the entry price rational relative to the market and future benchmarks?

- Entry price vs comparable units in the region

- Price vs nearby subsale and resale properties (99-yr normalised)

- Development staged pricing position

- Future GLS breakeven benchmark

S

Supply & Demand

Will there be a ready buyer pool when you are ready to exit?

- HDB upgrader pool size in the area

- Competing new condo supply pipeline

- Is this property better positioned than its competition?

E

Estate Appeal

Does the property have the physical attributes that sustain long-term demand?

- Development size — larger developments offer more liquidity at exit

- MRT, amenities, and preferred school proximity

- Efficient floor plan layout and usable space

- Facilities quality and development design

T

Transformation

Is the surrounding area set to improve — creating appreciation tailwinds aligned with your exit?

- Regional transformation (URA Master Plan)

- New MRT, malls, or schools in the pipeline

- Timing of transformation aligned with your target exit

Every shortlisted property gets scored. You see the numbers side by side so you make a confident, informed decision.

The highest-scoring property that meets your financial criteria is the recommendation — not the one that looks best on a show flat visit.

Made a shortlist but not feeling confident about your decision?

OUR BUYING PROCESS

|

OUR BUYING PROCESS |

From First Brief

to Keys in Hand.

You work directly with Ron & Ming Hui throughout the entire buying process — from financial assessment to offer strategy. No referrals to junior agents, no show flat ambushes. Just a disciplined, analytical process that keeps your interests — not the developer's — at the centre.

01

Financial Health Assessment

Know Exactly What You Can Afford — Before Anything Else

The first conversation is just that — a conversation. Ron maps your TDSR, CPF position, and monthly commitments to give you a clear, honest picture of your budget. No bank submissions, no credit checks, no commitment of any kind. You simply leave knowing your real numbers.

02

Buyer Brief & Goal Alignment

Tell Us What You Want — We'll Make Sure It's the Right Brief

Your timeline, preferred regions, property type, budget ceiling, and intended holding period are documented clearly before any research begins. This keeps the shortlist focused on what actually fits your life — not a generic range of options that wastes your weekends on show flats that were never right for you.

03

Macro & Micro Research

We Do the Research — You Review the Findings

Macro and micro research is done for you — regional price trends, URA transformation plans, supply pipeline, floor plan analysis, MRT proximity, and facilities assessment across all shortlisted options. By the time you visit a property, you already know whether it's worth your time.

04

ASSET SCORE COMPARISON

Compare Options Side by Side — in Numbers, Not Impressions

Every shortlisted property is scored across five dimensions using the ASSET framework, so you can compare them objectively. You're not choosing between two show flats based on which staging you liked more. You're choosing between two scored options — with the data in front of you.

05

CMA & Offer Strategy

Make an Offer With Confidence — Not Guesswork

A CMA on recent transactions for your target property confirms the safe entry price before any offer is made. Your ceiling and walk-away point are agreed with Ron beforehand — so there's no pressure, no second-guessing, and no overpaying because you fell in love with the unit at the wrong moment.

06

Completion

OTP Completion & Timeline Coordination

All OTP paperwork, legal coordination, and completion milestone tracking. For upgraders, the purchase timeline is coordinated with the HDB sale timeline to eliminate any gap or bridging loan requirement.

considering buying a new launch condo?

Navigate New Launches with Expert Guidance

New launches can be overwhelming. We're PropNex New Projects specialists—we know the ins and outs.

Start Your Buying Journey

Buy with Analysis.

Not Just a Feeling.

Start with a no-obligation consultation.

Your financial position assessed, your target options researched, and a shortlist scored with proven frameworks.

FAQs

How much cash do I actually need to buy a private condo in Singapore?

1

The minimum cash required depends on whether this is your first property or a subsequent one — but here is the baseline for a Singapore Citizen buying their first private condo with no outstanding property loans.

Your downpayment is 25% of the purchase price. A minimum 5% must be paid in cash — the remaining 20% can be paid via CPF Ordinary Account. On top of that, add Buyer's Stamp Duty (1–4% depending on price), legal fees (approximately $3,000–$5,000), and ideally a 12-month mortgage reserve fund. For a $1.5M condo, you are looking at approximately $75,000 in minimum cash, plus stamp duty of roughly $42,600, plus legal fees — so a realistic total cash outlay of around $125,000–$130,000 before CPF contributions.

What most buyers underestimate is the CPF accrued interest refund if they are upgrading from an HDB. Every dollar of CPF used for the HDB purchase — plus 2.5% interest compounded annually — must be returned to CPF upon sale. This reduces your cash-in-hand proceeds from the HDB sale and directly affects how much CPF is available for your condo purchase. Getting this modelled correctly before you start shortlisting properties is the most important financial step you can take.

Can I buy a private condo in Singapore if I still own an HDB flat?

2

Yes — Singapore Citizens are permitted to own both an HDB flat and a private property simultaneously, provided the HDB flat has fulfilled its 5-year Minimum Occupation Period (MOP). However, buying private property while still owning an HDB means you will pay 20% Additional Buyer's Stamp Duty (ABSD) on the private purchase at the time of transaction.

Most HDB upgraders avoid this by selling the HDB and purchasing the private property in close sequence — with the HDB sale completing within 6 months of the private purchase. This qualifies you for ABSD remission, effectively waiving the 20% duty. The sequencing of these two transactions is one of the most financially consequential decisions in the entire upgrade process, and getting it wrong can cost you tens of thousands of dollars in unnecessary stamp duty.

The right sequence depends on your HDB's MOP status, your CPF position, and the completion timeline of your target private property. This is mapped out explicitly at the start of every upgrade consultation with Own It — so you enter the process knowing the most cost-effective path before any commitment is made.

Should I buy a new launch or resale condo in Singapore?

3

Neither is universally better — and any agent who tells you otherwise without knowing your specific situation is giving you a pitch, not advice. The right answer depends on four things: your timeline, your financing structure, your intended holding period, and your exit strategy.

New launch condos offer modern layouts, brand-new facilities, a staged payment scheme (smaller upfront cash outlay during construction), and the potential for capital appreciation if you enter early in the right development. The trade-off: a 3–5 year wait until TOP, which means rental or temporary housing costs during construction — a significant hidden expense for upgraders using their HDB sale proceeds.

Resale condos offer immediate occupation, the ability to inspect the actual unit before purchase (not a show flat mock-up), and often better value per liveable square foot — particularly in older developments where unit sizes are more generous. They also offer cleaner financing for upgraders, since there is no construction risk and sale proceeds can be timed directly against completion.

The deciding factor for most upgraders is the financing structure. If your HDB sale proceeds need to fund the downpayment on the private property, a resale condo with a near-term completion is typically lower-risk than a new launch with a 4-year build period. Own It runs the comparison for both options through the ASSET scoring framework — so the decision is based on your actual numbers, not show flat impressions.

What should I look for when choosing a condo to buy in Singapore?

4

The most common mistake Singapore condo buyers make is starting with factors that feel important — developer brand, interior design, facilities — and ending with the financial analysis as an afterthought. The evaluation should work in the opposite direction.

Start with macro research: which region and district offers the strongest combination of demand drivers, URA transformation plans, and supply pipeline management? A condo in a well-positioned district will outperform a better-designed condo in a region with oversupply at exit.

Then move to micro research: floor plan efficiency before price per square foot. Singapore's newer condos have seen unit sizes shrink significantly — a lower headline price may conceal poor layout efficiency, void spaces, or a kitchen that cannot fit a standard oven. Study the floor plan before visiting the show flat, not after.

Finally, apply a consistent scoring framework across all shortlisted options. Own It uses the ASSET framework — five dimensions that score every property on Affordability, Safe Entry price, Supply and Demand, Estate Appeal, and Transformation potential. Every shortlisted property gets a comparable score so the final decision is made in numbers, not impressions. The highest-scoring property that meets your financial criteria is the recommendation — not the one with the nicest view from the show flat rooftop terrace.

How does ABSD work in Singapore, and is there a legal way to reduce it when buying a condo?

5

Additional Buyer's Stamp Duty (ABSD) is a tax levied on property purchases in Singapore above and beyond the standard Buyer's Stamp Duty. For Singapore Citizens, ABSD rates in 2025 are: 0% on your first residential property, 20% on your second, and 30% on your third and beyond. Permanent Residents pay 5% on their first property and 30% on their second. Foreigners pay 60% on any residential property purchase.

The most straightforward legal way for Singapore Citizens to reduce ABSD exposure is through sequenced upgrading — selling your HDB before or simultaneously with purchasing private property, so the private purchase qualifies as your first residential property at the time of transaction. HDB upgraders who complete their HDB sale within 6 months of the private purchase are eligible for ABSD remission.

For couples who already own private property and wish to purchase a second, decoupling — where one spouse legally transfers their share to the other, allowing the transferring spouse to purchase a new property as their "first" — remains a legal strategy in certain circumstances. However, the costs involved (stamp duty on the transfer, legal fees, refinancing) must be modelled against the ABSD savings to confirm it is financially worthwhile. This calculation is something Ron runs for every client considering a second property purchase — because the answer is highly situation-specific and the cost of getting it wrong is significant.